Research Article | DOI: https://doi.org/10.31579/2835-9291/004

Exploring the Role of Green Finance in Directly and Indirectly Mitigating CO2 Emissions: Evidence from China

- Lin Chen *

- Jingrong Tan

School of Economics. Zhejiang University of Technology 288 Liuhe Road, Xihu District, Hangzhou, 310013, China

*Corresponding Author: Lin Chen, School of Economics. Zhejiang University of Technology 288 Liuhe Road, Xihu District, Hangzhou, 310013, China

Citation: Lin Chen, Ai zhao, Jingrong Tan (2023). Exploring the Role of Green Finance in Directly and Indirectly Mitigating CO2 Emissions: Evidence from China. International Journal of Clinical Case Studies.2(1); DOI:10.31579/2835-9291/004

Copyright: © 2023 Lin Chen, This is an open-access article distributed under the terms of the Creative Commons Attribution License, which permits unrestricted use, distribution, and reproduction in any medium, provided the original author and source are credited.

Received: 03 January 2023 | Accepted: 26 January 2023 | Published: 30 January 2023

Keywords: green finance; CO2 emissions; influencing mechanism

Abstract

This study analyses the direct and indirect influences of green finance on CO2 emissions. Panel data from the 30 provinces in China covering 2000 - 2020 are used in this paper. The empirical results indicate that green finance not only directly reduces CO2 emissions, but also has indirectly impacts via the scale, technical, and structural effects. A comprehensive green finance investment policy for strengthening environmental responsibility and for funding green technology is necessary for a successful energy transition to meet China’s sustainable development goals.

1. Introduction

JEL classification codes:

Since opening up in the late 1980s and the deepening of reforms, China’s economy has developed at an annual rate of more than 9% in the subsequent 30 years (Wang et al., 2015; Chen et al., 2019). However, this economic growth has been attended by excessive energy utilization, resulting in high carbon dioxide (CO2) emissions that have caused increasingly severe environmental problems, such as air pollution and climate change (Kalkuhl and Wenz, 2020; Mukhtarov et al., 2022). Indeed, China has turned into the world’s largest energy consumer and biggest producer of CO2 (Xiao et al., 2017; Wu et al., 2022). In 2020, China accounted for 26.1% of global energy demand and 30.9% of global emissions, and its share of the world’s energy consumption is rising. Although the Chinese economy is the second largest in the world, it still lags behind developed economies in terms of environmental governance. How to balance economic development and environmental protection has thus become a pressing topic for scholars and policymakers.

Faced with international pressure to curb CO2 emissions and the consequences of domestic energy shortages and greenhouse gas emissions, the Chinese government has implemented a series of emission reduction measures. During the 11th Five-Year Plan (2006 - 2010) and 12th Five-Year Plan (2011-2015), China gained extraordinary headway in diminishing carbon intensity (measured as CO2 per unit of GDP). However, maintaining these gains is challenging in the post-COVID-19 period, since the accessibility and availability of green finance are assumed to have declined as financial strategies, government spending plans, and industry incomes come into question. (Taghizadeh-Hesary et al., 2021; Madaleno et al., 2022).

To aid sustainable economic development, the financial sector has launched financial instruments that explicitly target environmental assurance, such as green securities, green insurance, green bonds, and green credit card. Although China began to develop green finance in the 1990s, it was only in 2016 that the People’s Bank of China together with others provided the Guiding Opinions on Building a Green Finance System, which was the focus of the G20 summit in the same year.

Green finance has changed the traditional investment channel, as governments at all levels and financial institutions attach equal importance to economic and environmental benefits. In particular, green credit and green investment play a leading role in promoting sustainable economic development (Yao and Tang, 2021; Saeed Meo and Karim, 2022).

Thus, this study investigates the degree to which green finance influences CO2 emissions and proposes policy recommendations to achieve China’s emission reduction targets. Our main contributions are two-fold. First, despite the vast literature on the connections among CO2 emissions and green finance (Taghizadeh-Hesary et al., 2021; Gholipour et al., 2022; Sun and Chen, 2022), empirical studies on the influence mechanism between green finance and CO2 emissions are lacking. This study bridges this gap in the body of knowledge. Second, this study contributes to the mediating effect of green finance on CO2 emissions by analyzing the scale, technical, and structural effects.

The remainder of this paper is structured as follows, Section 2 presents the data used and experimental strategy. Section 3 presents and discusses the empirical findings. Section 4 presents the study’s conclusions and discusses the policy implications.

2. Variable Selection and Empirical Methodology

2.1. Variable selection and descriptions

We use the dependent variable of per capita CO2 emissions. The independent variable is green finance, which is constructed by the following four indices: green credit (the proportion of premium use in energy intensive industries), green investment (investment in environmental pollution control as a percentage of GDP), green insurance (the depth of agricultural insurance), and government support (the proportion of environmental protection expenditure) (Yang, Su, and Yao, 2021).

The control variables include the level of economic development (Shahbaz et al. 2013), energy consumption (Loures and Ferreira, 2019), urbanization level (Liang and Yang 2019), and population aging level (Liang and Yang 2019). Higher economic development, energy consumption, urbanization, and population aging correspond to higher CO2 emissions. Therefore, the signs of these variables are expected to be positive.

As the instrumental variables: In order to solve possible endogeneity problems, we select first and second order lag of independent variable following Zhou et al. (2022). In addition, we select economic size, technology level, and industry structure as the mediating variables to test how the scale, technical, and structural effects influence CO2 emissions (Dou et al. 2021). Table 1 presents the variable definitions, such as variable symbol and data source and Table 2 presents the descriptive statistics.

Note: Organized by the author

Note: Std.Dev. Denotes standard deviation.

2.2. Empirical model

A panel regression model is utilized or the estimation in this section. According to the regression stochastic effects of population, affluence, and technology model (Dietz and Rosa, 1997), population and economic movement are the two most significant factors affecting CO2 emissions. Further, studies have adopted such influencing factors as energy use (Ang, 2007; Farhani, Chaibi, and Rault, 2014; Doğan et al. 2022), and financial development (Kim, Wu, and Lin 2020). The multivariate framework used in this study is as follows:

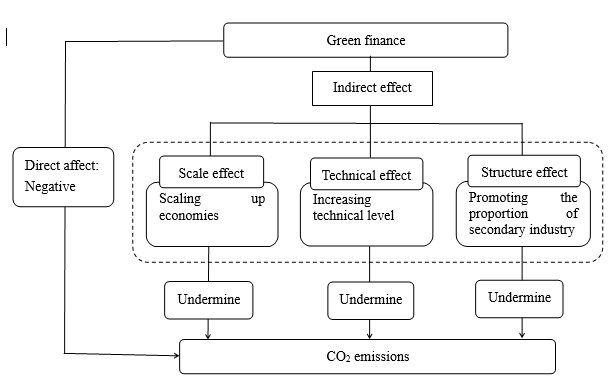

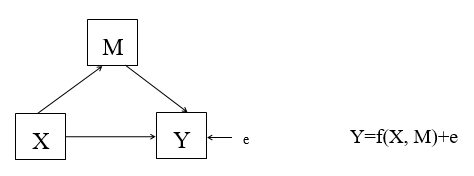

where i and t signify the province and year, respectively, and X denotes a vector of the control variables. In theory, policy instruments usually act on the final through the transmission of relevant mechanism variables (Zhou et al. 2022). The dependence variable is CO2 emissions, and green finance is a means to control CO2 emissions, while green finance needs to achieve the goal of reducing CO2 emissions through the mechanism variable M. α and γ respectively measure the marginal effect of green finance on β1 and mechanism variable M. If these two statistical coefficients are significant, then M can be considered as a mechanism for green finance to affect CO2 emissions. Eq.(5) is used to test the effect degree of mechanism M. In this study, mechanism variables M include economic scale, technology, and optimization of industrial structure, which represent scale effect, technology effect, and structure effect, respectively.

Different with Dou et al. (2021), we employ the economic scale to symbolize the scale effect instead of the total volume of imports and exports, and the total factor productivity (TFP) to symbolize the technical effect instead of the energy consumption intensity. Kalkuhl and Wenz (2020) suggested that annual gross product could measure the economy activity on the regional level. Lee and Lee (2022) suggested that TFP can be interpreted as a measure of technological change or technology dynamics.

3. Empirical Results

3.1. Estimation results

Table 3 shows the benchmark regression results. Per capita CO2 emissions are the dependent variable. First, with the OLS estimator results in Column [1], the coefficient of independent variable is significant at 1% level, except for urbanization level. Second, in order to control individual differences between provinces, we controls for the fixed effect, and excludes the control variables. The experimental results are displayed in Column [2]. Third, the control variables are gradually introduced into the model, and the regression results are shown in Columns [3] to [6]. We observe that the coefficient of green finance is significantly negative at the 1% level, showing that green finance significantly mitigates CO2 emissions. Moreover, a 1% improvement in the green finance level brings about a 0.3661% reduction in CO2 emissions (see Column (6)).

Hence, developing green finance is a viable strategy to mitigate CO2 emissions. In addition, the economic development level, energy consumption, urbanization level, and population aging level increase CO2 emissions, which are consistent with the findings of Balsalobre-Lorente et al. (2018), Pao and Tsai (2010), and Ajmi et al. (2013), who found that CO2 emissions are reduced by green finance and increased by energy consumption and economic growth.

Note: *** and * indicate statistical significance at 1% and 10% levels, respectively.

3.2. Robustness check

In this section, we check the robustness of the test results in three ways. First, we employ the FMOLS and FGLS estimators to repeat the regression in Section 3.1. Second, we set total CO2 emissions as the independent variable and employ OLS to estimate the variable coefficients. Finally, We also performed robustness analysis by applying 5Percentage bilateral tail indentation to the variables.

Table 4 shows that the coefficients of green finance are negative and significant, but with some differences. By the FMOLS and FGLS estimator, shown in Column (1) and (2), we find that increase in green finance mitigates in per capita CO2 emissions. Further, using the OLS estimator, a 1Percentage increase in green finance is associated with a 0.1271Percentage decrease in total CO2 emissions, shown in Column (3). Finally, employing the bilateral shrink tail, shown in Column (4), a 1Percentage increase in green finance is associated with a 0.2297Percentage decrease in per capita CO2 emissions. This analysis demonstrates that green finance can reduce CO2 emissions to a certain extent (Saeed Meo and Karim 2022).

Variable | FMOLS | FGLS | OLS_Total | Bilateral shrink tail |

| (1) | (2) | (3) | (4) |

lnGF | -0.6854*** (0.1125) | -0.7884*** (0.0354) | -0.1271** (0.0487) | -0.2297*** (0.0634) |

lnED | 0.4183*** (0.1106) | 0.5045*** (0.0293) | 0.1848** (0.0763) | 0.3148** (0.1175) |

lnEN | 0.4776*** (0.0621) | 0.1950*** (0.0170) | 0.6219*** (0.1025) | 0.3469** (0.1212) |

lnURB | 0.4539 (0.2985) | 0.6620*** (0.0675) | 0.0509 (0.1785) | 0.0448 (0.2780) |

lnAG | -0.3976*** (0.0346) | -0.0841*** (0.0108) | -0.0044** (0.0021) | -0.0057 (0.0037) |

_cons | -16.5806*** (1.0396) | -14.5920*** (0.2863) | -3.3443*** (0.6764) | -10.3215*** (0.8035) |

R2 | 0.3075 |

| 0.9058 | 0.8243 |

Obs. | 627 | 628 | 628 | 628 |

Table 4 Robustness results

Note:*** and ** indicate statistical significance at 1Percentage and 5Percentage levels, respectively.

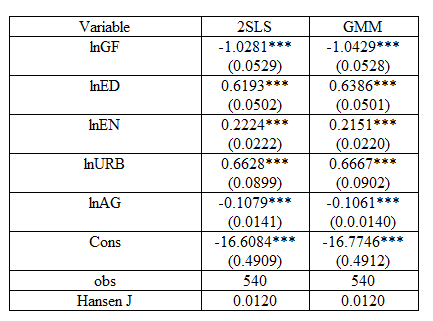

3.3 Endogeneity test

The above analysis provides a statistical basis for the development of green finance to mitigate CO2 emissions. When the level of emissions increase, green finance may be paid attention growth increase and the level of green finance will be improved. Therefore, there may be endogenous problems between green finance and CO2 emissions. In order to mitigate the potential endogeneity problems in the model, this study adopts two ways. First, we employ a series of control variables while assessing the model to reduce the opportunities for endogeneity resulting from overlooked factors. Second, we adopted the two-stage least squares (2SLS) and the GMM methods using instrumental variables.

Following past research (Bond, 1991; Yang et al., 2021), we utilize lagged green finance as instrumental variables in panel data. The used of lagged variables at time t-d fulfills the criteria of a valid instrumental variable, as they should be connected with the endogenous variable at time t, but are not associated with the error term at time t. Indeed, the independent variables of the lagging period are introduced to replace the informative factors of the on going time frame. Since the green finance level lagging behind the primary stage could antagonistically influence the green finance level in the last stage, this eliminates the influence of the ongoing stage somewhat, thereby subsequently reducing the issue of endogeneity.

As shown in Table 5, there are no significant differences between the magnitude and sign of the coefficient, indicating the robustness of the results. These results again show that the green finance level of the lagging term still mitigates CO2 emissions, consistent with the results of the baseline regression.

Through the above analysis, we conclude that green finance mitigates CO2 emissions, which is consistent with the findings of Saeed Meo and Karim (2022) and Mamun, Boubaker, and Nguyen (2022). We further analyse the influencing mechanism of this relationship through the scale, technical, and structural effects in Section 3.4.

Table 5 Endogeneity test

Note:*** indicates statistical significance at 1Percentage levels.

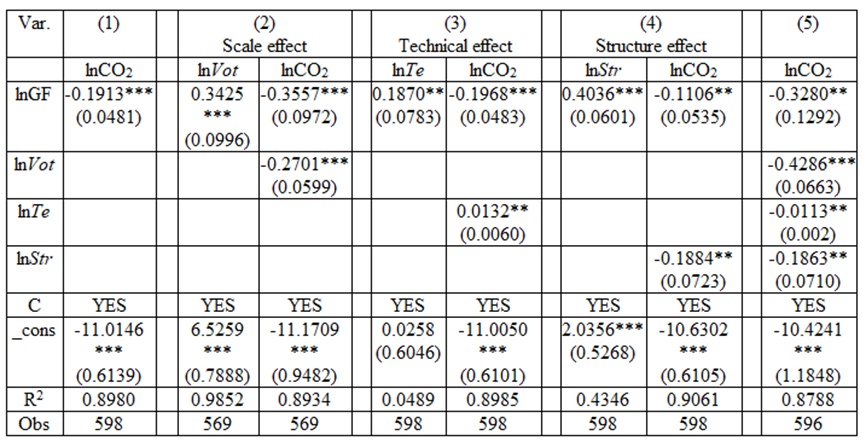

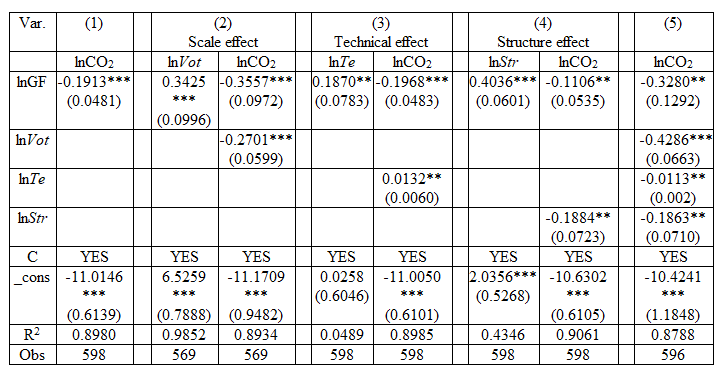

3.4 Influencing mechanism test

The mechanism effect results in Table 6 show that green finance mitigates CO2 emissions through all three effects. Thus, green finance and CO2 emissions have a significant negative correlation (Mamun, Boubaker, and Nguyen 2022).

For the scale effect, expanding green finance significantly increases economic size and decreases CO2 emissions. When the other factors are held constant, economic size increases by 0.3425Percentage for every 1Percentage increase in green finance. Through the mediating effect of economic size, the marginal impact of green finance on CO2 emissions rises. Specifically, the continued extension of green finance practices may increase economic performance by increasing economies of scale (Srivastava et al. 2020; Yang et al. 2021). In developing countries, when economies have grown, emissions have fallen (Narayan, Saboori, and Soleymani 2016; Narayan and Narayan 2010).

For the technical effect, the results indicate that green finance increases technological efficiency and reduces CO2 emissions, consistent with the results of Y. Wang et al. (2021). According to the results in Column [3], a 1Percentage improvement in green finance, translates into a 6Percentage improvement in technology. Although the coefficient of technological progress is positive, the value is very low. To mitigate CO2 emissions, the production process should be improved by investing in technological innovation and capital stocks (Shahbaz et al. 2019).

For the structural effect, increasing green finance can significantly increase the proportion of the secondary industry, which can help reduce CO2 emissions according to Xiao et al. (2017). Advanced technology and abundant financial assets brought about by green finance provide an opportunity for the secondary industry to develop low-carbon technologies (Dou et al. 2021). The results in Column [4] show that the marginal impact of green finance is smaller than expected, which is not consistent with the desired result.

In Column [5], we consider economic size, technological level and industrial structure, simultaneously. The marginal impact of green finance on reducing carbon emissions is 0.3280Percentage. To summarize, green finance not only directly decreases CO2 emissions, but also lowers such emissions indirectly through the scale, technical, and structural effects.

Table 6 Results of the mediating effects in the green finance-CO2 nexus

Note: The value in parentheses represent Std.Err. ***indicate statistical significance at 1Percentage level. ** indicate statistical significance at 5Percentage level.

C include control variables.

4. Conclusions and Policy Implications

In this study, using panel data from the 30 provinces in China covering 2000 - 2020 to assess the influence of green finance on CO2 emissions, the outcomes led to two main findings: First, green finance directly reduces CO2 emissions. Second, green finance promotes economic development, technology development and the optimization of the industrial structure, and then reducing CO2 emissions. In summary, concurring with Madaleno, Dogan, and Taskin (2022), a comprehensive green finance investment policy for strengthening environmental responsibility and funding green technology is necessary for successful energy transition and to meet China’s sustainable development goals. However, it is important to reinforce the supervision of green finance to accomplish the country’s emission reduction targets.

Based on the findings above, several policy implications are highlighted as follow. First, green finance mitigates of CO2 in China. Thus, to jointly achieve a carbon reduction target, it will be necessary to encourage and regulate green finance in China. More specifically, the government should promote green financial knowledge and guide the circulation of green financial assets. Second, through the mechanism effect analysis, scale effect and technological effect are conductive to mitigate CO2 emissions, which indicate that policy makers should develop economic and technology by green finance. Additionally, governors should think highlight of the industrial structure and encourage second industry to instead the high energy consumption, high emission, and high pollution industry.

Although this study has demonstrated that development green finance mitigate emissions of CO2 in China, some limitations still exist. While, the environmental policy, green finance development, and economic development are different in each province. However, this study has not discussed each province’s green finance-CO2 relationships separately. Thus, in future research, it could aim at environmental policies and green financial instruments in different regions, the impacts of green finance on carbon emissions under different backgrounds are analyzed more specifically.

Author statement

Jingrong Tan: Funding acquisition, Conceptualization, Methodology, Visualization, and Software.

Lin Chen: Conceptualization, Supervision, Validation, Investigation,Writing-Original draft preparation and Editing.

Acknowledgments

We gratefully acknowledge the Nation Social Science Foundation of China (No.C1310200211, Research on the mechanism and realization path of the coupling linkage between China’s economic resilience and high trade quality under the new situation of Sino-US trade relations) and Major Projects of the National Social Science Foundation (No.18ZDAO67, Research on the mechanism and implementation path of coordinated development of China’s industrial and trade policies in the new era). We would like to thank Dr. An Hu and Xiaojie Zhou for their useful comments. We are of course responsible for all errors and omissions. The views expressed in this paper are those of the authors and do not necessarily represent the views of their affiliated institutions. The authors declare that they have no known competing financial interests or personal relationships that could have appeared to influence the work reported in this paper.

References

- Ajmi, Ahdi Noomen, Shawkat Hammoudeh, Duc Khuong Nguyen, and João Ricardo Sato. (2013). “On the Relationships between CO2 Emissions, Energy Consumption and Income: The Importance of Time Variation.” Energy Economics 49:629–638.

View at Publisher | View at Google Scholar - Ang, James B. (2007). “CO2 Emissions, Energy Consumption, and Output in France.” Energy Policy 35(10):4772–4778.

View at Publisher | View at Google Scholar - Balsalobre-Lorente, Daniel, Muhammad Shahbaz, David Roubaud, and Sahbi Farhani. (2018). “How Economic Growth, Renewable Electricity and Natural Resources Contribute to CO2 Emissions?” Energy Policy 113(November 2017):356–367.

View at Publisher | View at Google Scholar - Bond, Stephen. (1991). “Some Tests of Specification for Panel Data:Monte Carlo Evidence and an Application to Employment Equations.” Review of Economic Studies 58(2):277–297.

View at Publisher | View at Google Scholar - Chen, Yulong, Jincai Zhao, Zhizhu Lai, Zheng Wang, et al. 2019. “Exploring the Effects of Economic Growth, and Renewable and Non-Renewable Energy Consumption on China’s CO2 Emissions: Evidence from a Regional Panel Analysis.” Renewable Energy 140:341–353.

View at Publisher | View at Google Scholar - Dietz, Thomas, and Eugene A. Rosa. (1997). “Effects of Population and Affluence on CO2 Emissions.” Proceedings of the National Academy of Sciences of the United States of America 94(1):175–179.

View at Publisher | View at Google Scholar - Doğan, Buhari, Lan Khanh Chu, Sudeshna Ghosh, Huong Hoang Diep Truong, et al. (2022). “How Environmental Taxes and Carbon Emissions Are Related in the G7 Economies?” Renewable Energy 187:645–656.

View at Publisher | View at Google Scholar - Dou, Yue, Jun Zhao, Muhammad Nasir, and Kangyin Dong. (2021). “Assessing the Impact of Trade Openness on CO 2 Emissions: Evidence from China-Japan-ROK FTA Countries.” Journal of Environmental Management 296:113241.

View at Publisher | View at Google Scholar - Gholipour, Hassan F, Amir Arjomandi, and Sharon Yam. (2022). “Green Property Finance and CO2 Emissions in the Building Industry.” Global Finance Journal 51, 100696.

View at Publisher | View at Google Scholar - Kalkuhl, Matthias, and Leonie Wenz. (2020). “The Impact of Climate Conditions on Economic Production. Evidence from a Global Panel of Regions.” Journal of Environmental Economics and Management 103(603864):102360.

View at Publisher | View at Google Scholar - Kim, Dong Hyeon, Yi Chen Wu, and Shu Chin Lin. (2020). “Carbon Dioxide Emissions and the Finance Curse.” Energy Economics 88.

View at Publisher | View at Google Scholar - Lee, Chi Chuan, and Chien Chiang Lee. (2022). “How Does Green Finance Affect Green Total Factor Productivity? Evidence from China.” Energy Economics 107, 105863.

View at Publisher | View at Google Scholar - Liang, Wei, and Ming Yang. (2019). “Urbanization, Economic Growth and Environmental Pollution: Evidence from China.” Sustainable Computing: Informatics and Systems 21:1–9.

View at Publisher | View at Google Scholar - Loures, L., and P. Ferreira. (2019). “Energy Consumption as a Condition for per Capita Carbon Dioxide Emission Growth: The Results of a Qualitative Comparative Analysis in the European Union.” Renewable and Sustainable Energy Reviews 110: 220–225.

View at Publisher | View at Google Scholar - Madaleno, Mara, Eyup Dogan, and Dilvin Taskin. (2022). “A Step Forward on Sustainability: The Nexus of Environmental Responsibility, Green Technology, Clean Energy and Green Finance.” Energy Economics 109: 105945.

View at Publisher | View at Google Scholar - Mamun, Md Al, Sabri Boubaker, and Duc Khuong Nguyen. (2022). “Green Finance and Decarbonization: Evidence from around the World.” Finance Research Letters 46(PB):102807.

View at Publisher | View at Google Scholar - Mukhtarov, Shahriyar, Serhat Yüksel, and Hasan Dinçer. (2022). “The Impact of Financial Development on Renewable Energy Consumption: Evidence from Turkey.” Renewable Energy 187:169–176.

View at Publisher | View at Google Scholar - Narayan, Paresh Kumar, Behnaz Saboori, and Abdorreza Soleymani. (2016). “Economic Growth and Carbon Emissions.” Economic Modelling 53:388–397.

View at Publisher | View at Google Scholar - Pao, Hsiao Tien, and Chung Ming Tsai. (2010). “CO2 Emissions, Energy Consumption and Economic Growth in BRIC Countries.” Energy Policy 38(12):7850–7860.

View at Publisher | View at Google Scholar - Saeed Meo, Muhammad, and Mohd Zaini Abd Karim. (2022). “The Role of Green Finance in Reducing CO2 Emissions: An Empirical Analysis.” Borsa Istanbul Review 22(1):169–178.

View at Publisher | View at Google Scholar - Shahbaz, Muhammad, Giray Gozgor, Philip Kofi Adom, and Shawkat Hammoudeh. (2019). “The Technical Decomposition of Carbon Emissions and the Concerns about FDI and Trade Openness Effects in the United States.” International Economics 159: 56–73.

View at Publisher | View at Google Scholar - Shahbaz, Muhammad, Qazi Muhammad Adnan Hye, Aviral Kumar Tiwari, and Nuno Carlos Leitão. (2013). “Economic Growth, Energy Consumption, Financial Development, International Trade and CO2 Emissions in Indonesia.” Renewable and Sustainable Energy Reviews 25:109–121.

View at Publisher | View at Google Scholar - Srivastava, Anup Kumar, Mridul Dharwal, and Aarti Sharma. 2020. “Green Financial Initiatives for Sustainable Economic Growth: A Literature Review.” Materials Today: Proceedings 49:3615–3618.

View at Publisher | View at Google Scholar - Sun, Haiyan, and Fushan Chen. (2022). “The Impact of Green Finance on China’s Regional Energy Consumption Structure Based on System GMM.” Resources Policy 76: 102588.

View at Publisher | View at Google Scholar - Taghizadeh-Hesary, Farhad, Naoyuki Yoshino, and Han Phoumin. (2021). “Analyzing the Characteristics of Green Bond Markets to Facilitate Green Finance in the Post-Covid-19 World.” Sustainability (Switzerland) 13(10).

View at Publisher | View at Google Scholar - Wang, Shaojian, Chuanglin Fang, Yang Wang, Yongbin Huang, et al. (2015). “Quantifying the Relationship between Urban Development Intensity and Carbon Dioxide Emissions Using a Panel Data Analysis.” Ecological Indicators 49:121–131.

View at Publisher | View at Google Scholar - Wu Yizhen, Chuanlong Li, Kaifang Shi, Shirao Liu, and Zhijian Chang. (2022). “Exploring the Effect of Urban Sprawl on Carbon Dioxide Emissions: An Urban Sprawl Model Analysis from Remotely Sensed Nighttime Light Data.” Environmental Impact Assessment Review 93:106731.

View at Publisher | View at Google Scholar - Xiao, Bowen, Dongxiao Niu, and Han Wu. (2017). “Exploring the Impact of Determining Factors behind CO2 Emissions in China: A CGE Appraisal.” Science of the Total Environment 581–582:559–572.

View at Publisher | View at Google Scholar - Yang, Ting, and Qiang Wang. (2020). “The Nonlinear Effect of Population Aging on Carbon Emission-Empirical Analysis of Ten Selected Provinces in China.” Science of the Total Environment 740:140057.

View at Publisher | View at Google Scholar - Yang, Yuxue, Xiang Su, and Shuangliang Yao. (2021). “Nexus between Green Finance, Fintech, and High-Quality Economic Development: Empirical Evidence from China.” Resources Policy 74:102445.

View at Publisher | View at Google Scholar - Yao, Xingyuan, and Xiaobo Tang. (2021). “Does Financial Structure Affect CO2 Emissions? Evidence from G20 Countries.” Finance Research Letters 41(2):101791.

View at Publisher | View at Google Scholar - Zhou, Guangyou, Jieyu Zhu, and Sumei Luo. (2022). “The Impact of Fintech Innovation on Green Growth in China: Mediating Effect of Green Finance.” Ecological Economics 193:107308.

View at Publisher | View at Google Scholar - Zhou, Hongji, and Guoyin Xu. (2022). “Research on the Impact of Green Finance on China’s Regional Ecological Development Based on System GMM Model.” Resources Policy 75:102454.

View at Publisher | View at Google Scholar